The SEC opened 2026 filing three separate insider trading cases in life sciences within a month. Each case targets a different participant. Have questions? Spotted an interesting data trend? Just want to chat about what we're building? → Drop me a line at BUILDING QUIVER FOR YOUGot 90 seconds? Tell us what features you want, report a bug, or let us know what is working. Every response gets read.

If you find value in what we're doing, please

(yes, even your mom who keeps asking what stocks to buy).

On January 26, the

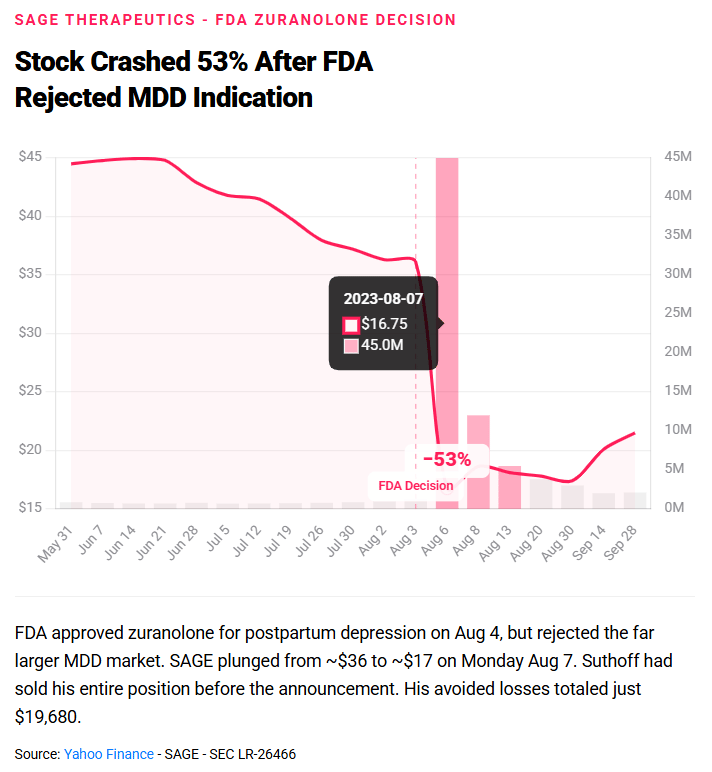

against Brian Suthoff, a Massachusetts resident who sold his entire position in Sage Therapeutics

after learning from a company insider that the FDA had struck major depressive disorder from the proposed label of Sage's flagship drug, zuranolone. Suthoff had held those shares for more than two years. He dumped them right before Sage announced the FDA's decision on August 4, 2023. The stock fell 53%. His avoided losses: $19,680.

For $19,680 in avoided losses, the SEC deployed the full weight of a federal enforcement action. The threshold for enforcement is not about how much you made. It's about whether you traded on material nonpublic information at all. The message to biotech insiders: there is no amount small enough to fly under the radar.

On January 15, the

Hong "John" Wang and his consulting firm, Precision Clinical Consulting, with insider trading in C4 Therapeutics stock. Wang was performing biostatistical analysis on C4's

flagship cancer drug when he accessed positive clinical trial data before the public announcement. He bought shares between November and December 2023. When C4 announced the results, the stock doubled. His profits: over $450,000 in realized and unrealized gains.

What makes the Wang case interesting isn't the trade itself. It's the compliance paper trail. C4 had an insider trading policy. Wang signed a consulting agreement that explicitly prohibited using confidential information outside his work duties. He completed mandatory training that identified clinical trial results as an example of potential MNPI. He acknowledged in writing that federal law restricted his ability to trade. Then he traded.

The Wang case matters because it demolishes the compliance defense. Every safeguard a public company is supposed to have in place was in place. Wang signed everything. He trained on everything. He acknowledged everything. And none of it stopped him. The case is now Exhibit A for why the SEC considers compliance paperwork necessary but insufficient. If the person filling out the forms is the same person trading the stock, the forms are theater.

he blew through, which reads less like an enforcement action and more like a compliance department's autopsy report. On

On January 6, the

, Muhammad Saad, Arham, and Shahwaiz Shoukat, along with three associates, in a scheme that makes the first two cases look like parking tickets. The operation involved insider trading on nine pharmaceutical acquisitions, two separate stock manipulation campaigns, impersonation of physicians, fabrication of clinical trial data, and distribution of fake press releases through legitimate news wires.

Total profits across the ring: approximately $41 million. Here's how the insider trading worked. Gyunho "Justin" Kim, an investment banker in Citigroup's (C) San Francisco healthcare M&A group, allegedly tipped Saad Shoukat with deal intelligence on nine upcoming acquisitions.

Those included Pfizer's

$5.4 billion purchase of Global Blood Therapeutics, AbbVie's

$10.1 billion buyout of ImmunoGen, and deals involving Amgen

, Biogen

, and (

). Saad passed the tips to his brothers and two friends, Izunna Okonkwo and Daniyal Khan. They traded ahead of each announcement.

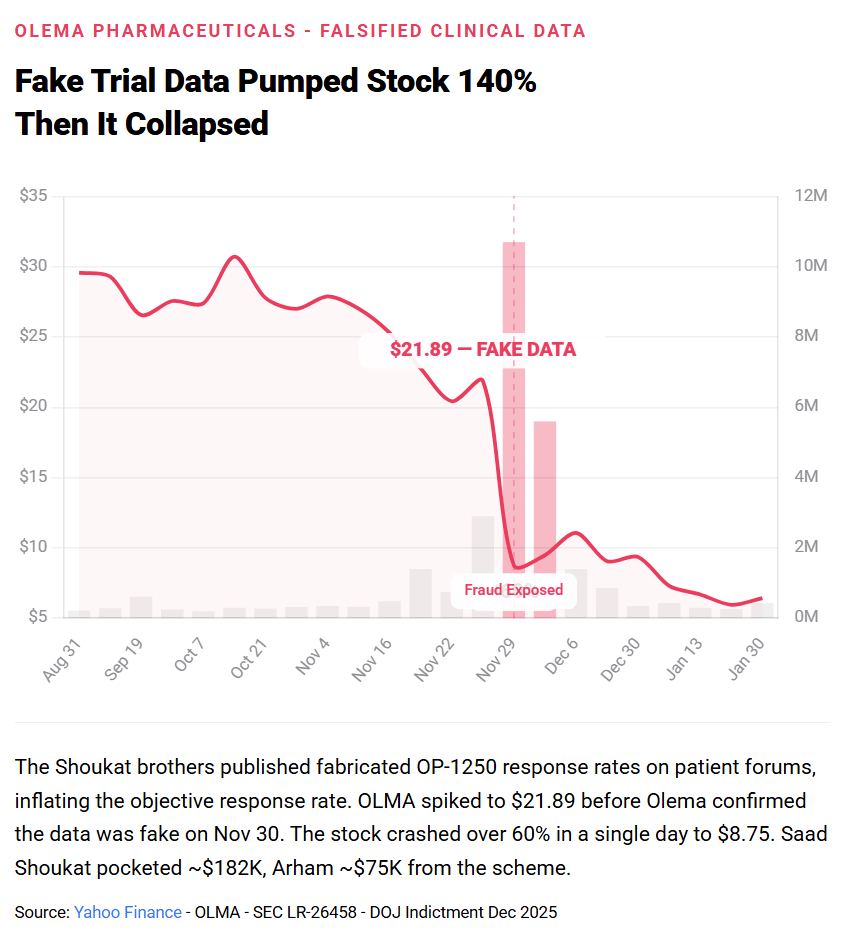

In a separate scheme involving Olema Pharmaceuticals

, the brothers went further. Saad and Arham invested in Olema, which was developing OP-1250, a breast cancer treatment in Phase I/II trials. They then allegedly impersonated physicians, adopting pseudonyms like "Dr. Joseph Garza" and using spoofed email accounts mimicking oncology hospitals including Texas Oncology, Roswell Park Comprehensive Cancer Center, and Ackerman Cancer Center, to extract confidential efficacy and safety data from Olema.

When the data showed the drug was less effective than they wanted, they fabricated favorable results, published them on cancer patient forums under stolen identities of metastatic breast cancer patients, and rode the stock spike. Olema issued a statement that the data was falsified. The brothers had already sold.

They impersonated oncologists. They stole breast cancer patient identities. They fabricated clinical data for a drug real patients were waiting on. They issued fake press releases through real news wires. And they are currently being represented by former New Jersey governor Chris Christie.

Biotech is uniquely dangerous for insider trading because the material nonpublic information is binary. The drug works or it doesn't. The FDA approves or it doesn't. The acquisition closes or it doesn't. That makes the edge from early knowledge mathematically cleaner than in almost any other sector, and it makes the temptation proportionally larger. The SEC seems to understand this. Nearly every public company enforcement action in early 2026 involves pharmaceutical disclosures or life sciences data. If your alpha comes from knowing what the FDA is about to say, the SEC has made its position explicit: that's not alpha, it's probable cause.

Quiver makes the information gap visible. Pull insider trading data on SAGE, C4 Therapeutics, Olema, and Opiant to compare legitimate insider transactions against the suspicious trading windows identified in the SEC complaints. Then check congressional trading in healthcare and biotech names around major FDA calendar dates. The same binary catalysts that attract fraud also attract political attention, and Quiver tracks both.