Risk Factors Dashboard

Once a year, publicly traded companies issue a comprehensive report of their business, called a 10-K. A component mandated in the 10-K is the ‘Risk Factors’ section, where companies disclose any major potential risks that they may face. This dashboard highlights all major changes and additions in new 10K reports, allowing investors to quickly identify new potential risks and opportunities.

View risk factors by ticker

Search filings by term

Risk Factors - TALO

-New additions in green

-Changes in blue

-Hover to see similar sentence in last filing

Reserve engineering is a process of estimating underground accumulations of oil, natural gas and NGLs that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions made by reserve engineers. In addition, the results of drilling, testing and production activities may justify upward or downward revisions of estimates that were made previously. If significant, such revisions would change the schedule of any further production and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil, natural gas and NGLs that are ultimately recovered.

Should one or more of the risks or uncertainties described herein occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements. All forward-looking statements, expressed or implied, included in this report are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue. Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this report.

6

SUMMARY RISK FACTORS

Risks Related to our Business and the Oil and Natural Gas Industry

7

Risks Related to our Capital Structure and Ownership of our Common Stock

|

| • | Resolution of litigation could materially affect our financial position and results of operations. |

8

Part I

Items 1 and 2. Business and Properties

Overview

As used in this Annual Report on Form 10-K (this “Annual Report”) and unless otherwise indicated or the context otherwise requires, references to “we,” “us,” “our,” “Talos Energy Inc.,” “Talos” and the “Company” refer to, from and after the Stone Closing (as defined below), Talos Energy Inc. and its consolidated subsidiaries and prior to the Stone Closing, Talos Energy LLC and its consolidated subsidiaries.

We were incorporated on November 14, 2017 under the laws of the state of Delaware for the purpose of effecting the business combination between Talos Energy LLC and Stone Energy Corporation (“Stone”), pursuant to which each of Talos Energy LLC and Stone became our wholly-owned subsidiary. We refer to this business combination as the “Stone Combination,” and its date of consummation, May 10, 2018, as the “Stone Closing Date.”

We are a technically-driven independent offshore energy company engaged in oil and gas exploration and production in the U.S. Gulf of Mexico and offshore Mexico. We are focused on safely and efficiently maximizing value through our operations. We leverage decades of geology, geophysics and offshore operations expertise towards the acquisition, exploration, exploitation and development of assets in key geological trends that are present in many offshore basins around the world.

We combine our technical experience in geology, geophysics and engineering with innovative resource evaluation techniques and seismic imaging expertise to discover new resources. We rely on our operational experience to safely and responsibly optimize production and recovery from our assets. Finally, we leverage our commercial and corporate management experience to most effectively allocate our capital to balance risk and reward, grow our business and maximize long-term shareholder value.

Prior to the Stone Combination, Talos Energy Inc. had not conducted any material activities other than those incident to its incorporation and certain matters contemplated by that certain transaction agreement, dated as of November 21, 2017 (the “Stone Transaction Agreement”) by and among Stone, Talos Energy Inc., Sailfish Merger Sub Corporation (“Merger Sub”), Talos Energy LLC (which was renamed to Talos Energy Inc. and converted into a Delaware corporation after the Stone Combination) and Talos Production LLC (which was converted into a Delaware corporation named Talos Production Inc. in 2019), pursuant to which, among other items, each of Stone, Talos Production LLC and Talos Energy LLC became wholly-owned subsidiaries of Talos Energy Inc. The Stone Combination was accounted for as a business combination in accordance with accounting principles generally accepted in the United States of America (“GAAP”), with Talos Energy LLC treated as the “acquirer” and Stone treated as the “acquired” company for financial reporting purposes. Accordingly, the reported financial condition and results of operations of the Company reflect the assets, liabilities and results of operations of Talos Energy LLC (as our predecessor) prior to the Stone Combination, and do not reflect the assets, liabilities and results of operations of Stone prior to such date. The assets, liabilities and results of operations of Talos Energy LLC have not been, and will not be, restated retrospectively to reflect the historical financial position or results of operations of Stone.

For more information on Talos Energy LLC, our predecessor for financial reporting purposes, see Part IV, Item 15. Exhibits, Financial Statement Schedules — Note 1 — Formation and Basis of Presentation.

Business Strategy

We intend to increase stockholder value by growing our reserves, production, cash flow and future growth opportunities in a capital efficient manner. Our core competencies of deep technical expertise and extensive offshore operating experience allow us to successfully manage our asset base and consistently make attractive investments, thereby increasing shareholder value over time.

We maintain a large and diverse in-house technical staff focused on geology, geophysics, engineering and other technical disciplines, providing many decades of exploration and production experience in key resource trends where we focus. Our significant library of seismic data resources, which focuses on the U.S. Gulf of Mexico and offshore Mexico, allows our technical team to apply proprietary seismic reprocessing techniques to evaluate or re-evaluate potential resources across our asset portfolio. Finally, we have deep in-house experience across our offshore operations, production operations, safety, facilities and business development.

9

Our strategic business development activities allow us to consistently identify and evaluate new opportunities through a wide range of potential avenues, including government lease sales, joint ventures and acquisitions, among others. Our proven track record through the drill bit frequently attracts potential drilling partners in projects that we operate, while in non-operated projects we leverage our core competencies to independently identify the best investment opportunities, review partner-proposed projects and be a value-added contributor. Finally, our asset acquisition strategy is focused on assets with a geological setting that can benefit from our ability to use our seismic database and technical expertise to re-evaluate and improve the acquired properties. Specifically, our acquisition focus areas target a variety of potential situations and sellers that are currently available in offshore basins, including single asset acquisitions, consolidation of private companies and broader asset package transactions. We seek to actively participate in government lease sales to identify and acquire attractive leasehold acreage, which in many cases has not been evaluated with the latest reprocessed seismic data, resulting in an opportunity for us to identify previously unknown drilling prospects.

We have historically focused our operations in the U.S. Gulf of Mexico because of our deep experience and technical expertise in the basin, which maintains favorable geologic and economic conditions, including multiple reservoir formations, comprehensive geologic and geophysical databases, extensive infrastructure and an attractive and asset acquisition market. Utilizing our core competencies in conjunction with a robust and active business development effort allows us to use the following strategies to increase stockholder value:

Continuously Optimizing our Attractive Existing Asset Base.

We benefit from our proven ability to enhance and extend the life of existing projects within our portfolio. Investments in optimization projects across our asset base aim to stabilize and improve the profile of producing assets by increasing recovery, production and cash flow with typically relatively low investment capital and risk. These projects allow for reinvestment opportunities in exploitation and exploration projects.

Conducting Development and Near-Field Projects In and Around Our Existing Asset Footprint.

We undertake asset development and exploitation drilling projects in close proximity to our existing assets as well as facilities that we either own or have access to. These projects leverage ongoing operations and existing technical knowledge of the area, often coupled with recent proprietary seismic reprocessing evaluations to provide attractive incremental investment opportunities to grow reserves, production and cash flow in well-understood areas.

Our asset footprint, which includes operational control of several key shallow and deepwater facilities, allows us to invest in a diverse set of opportunities ranging from in-field development to high impact exploration projects while optimizing our facilities to lower incremental operating costs structures. We also believe our operated infrastructure can be attractive to other operators looking for a host facility for their subsea tie-back projects, which allows us either to be involved in new investment opportunities or to offset the operating cost of these facilities with fee-based income earned by hosted third-party production.

Engaging in Exploration Activities to Grow Asset Base and Potentially Unlock Significant New Resources.

We conduct exploration drilling activities across our acreage set with risk-weighted investments that could establish significant new reserves and production. These projects are intended to optimize risk and reward across our portfolio of prospective drilling opportunities by finding and developing previously undiscovered resources along existing or emerging geological trends with the most efficient deployment of capital. When successful, exploration drilling activities can organically generate material new assets for the Company.

10

Utilize Acquisitions and Other Business Development Activities to Expand Asset Base, Opportunity Set and Value Creation Potential.

We rely on our commercial and business development activities to expand our asset base through the acquisition or optimization of additional or existing properties, respectively. Commercial and business development provides a key avenue to create additional value from the acquisition of undervalued properties where we can apply our technical and operational competencies to generate upside. Additionally, we utilize business development to acquire new leaseholds, enter new projects and increase or decrease working interests in various existing projects to optimize capital planning and our targeted risk/return profile for varying business conditions. Consolidation opportunities in our basin and, more broadly, in the offshore exploration and production segment in other basins around the world, are numerous and span a wide range of lifecycle stages, sizes and geographic variables. We expect to continue utilizing acquisitions and business development to grow our business in a manner that preserves a strong and healthy credit profile as well as a diverse and high-quality asset base.

Maintain Safety, Environmental Responsibility and Sustainability as Key Principles for Operations Across All Areas of our Business.

We are focused on maintaining high standards of safety, environmental responsibility and corporate citizenship across all elements of our business. We closely monitor safety performance and consistently take steps to improve our performance. For the year ended 2020, we were able to maintain a high level of safety performance with a lower recordable incident rate when compared to the average for offshore operators in the U.S. Gulf of Mexico and as well as across numerous other industrial sectors of the broader economy. We strive to execute our business plan while simultaneously minimizing our environmental footprint, including emissions, potential spills and other impacts. Due to the nature of subsea wells and ample offshore pipelines, we believe the offshore operating environment is a region where greenhouse gas (“GHG”) emissions can continue to be lowered over time. Finally, we aim to be a good corporate citizen in the regions and communities where we operate. We recently published our inaugural Environmental Social and Governance (“ESG”) report highlighting our performance and initiatives across all of these categories and other topics.

Properties

United States Gulf of Mexico

Our area of focus in the United States is the Gulf of Mexico deepwater, which is generally considered to comprise water depths over 600 feet. Our strategy is focused in areas characterized by clearly defined infrastructure, well-known production history and geological well control, which reduces operational and investment risk. We believe the potential for large discoveries and increasing success rates in the sub-salt and mini-basin lower Pliocene and Miocene plays has resulted in increased industry focus on this area over the last decade.

We believe our deepwater operations in the U.S. Gulf of Mexico provide significant potential growth opportunities through our planned drilling program. Through our technical approach of starting with known hydrocarbon systems and applying modern seismic reprocessing techniques, we have generated a substantial inventory of deepwater prospects that we believe are capable of delivering predictable production growth. We primarily focus our exploitation and exploration efforts around our existing infrastructure. This subsea tie-back strategy allows for better project economics and shorter periods between a discovery and production.

11

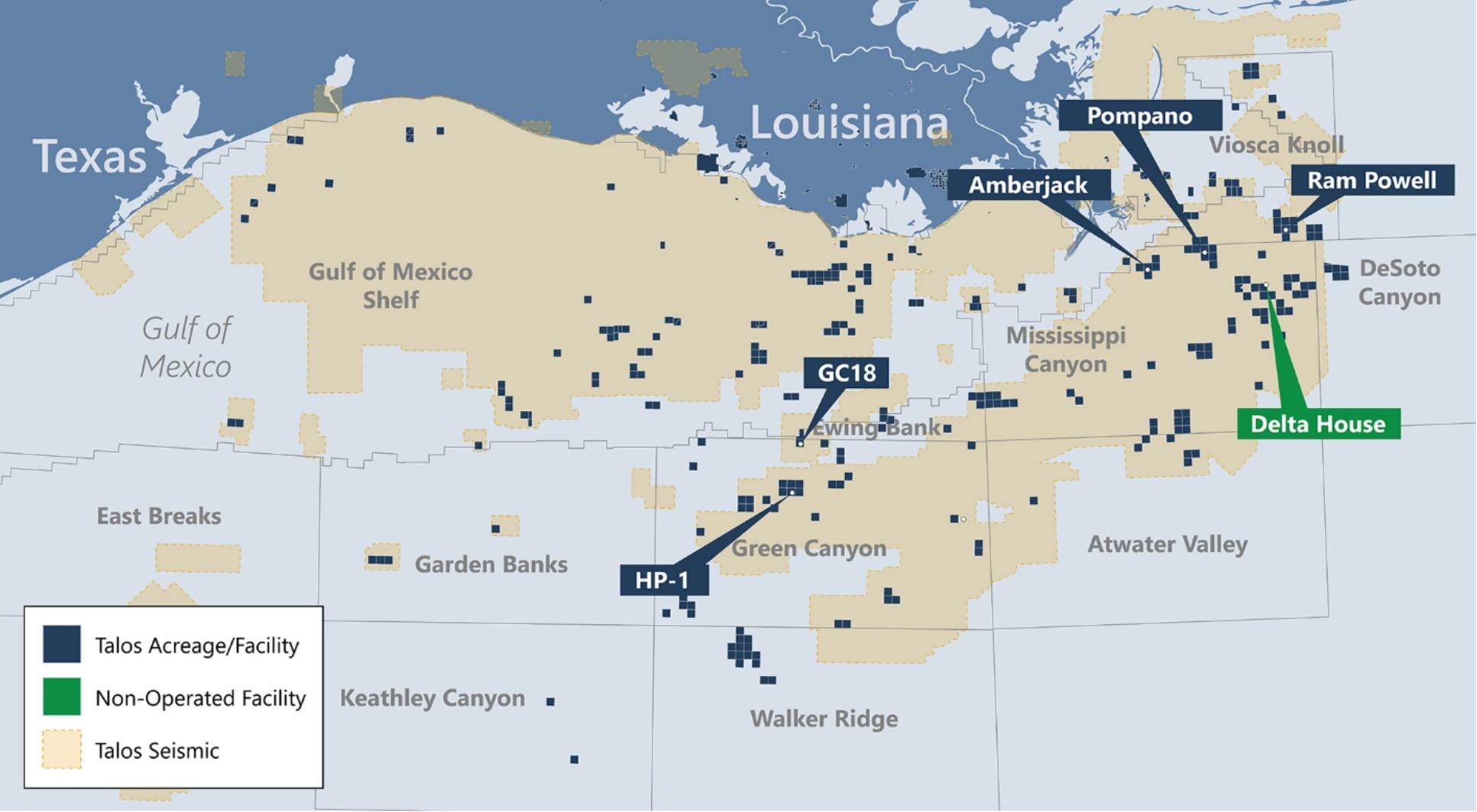

As of December 31, 2020, our core areas in the United States are illustrated below:

The following table sets forth a summary of certain key 2020 information regarding our core areas in the United States:

Green Canyon — Green Canyon is a deepwater region in the Central U.S. Gulf of Mexico and is a key focus area both industry-wide and for our exploration activities. We operate two production facilities in the region, including a floating production unit, the Helix Producer I (“HP-I”).

Mississippi Canyon — Mississippi Canyon is a deepwater region in the eastern portion of the Central U.S Gulf of Mexico with a track record of prolific production and ongoing exploration success that continues to unlock new resources. We operate three production facilities in the region and are active as both an operator and non-operating partner in numerous development projects and producing fields.

Shelf and Gulf Coast — The U.S. Gulf of Mexico Shelf (the “Shelf”) and Gulf Coast (“Gulf Coast”) area spans an enormous geographical area across the basin and provides diverse production from numerous operated production facilities. The Shelf area is a producing region of the basin with attractive redevelopment, recovery enhancement and exploration opportunities.

Mexico

Our areas of focus in Mexico are blocks located within the Sureste Basin, a prolific proven hydrocarbon province, in the shallow waters off the coast of Mexico’s Veracruz and Tabasco states. We have executed Production Sharing Contracts (“PSCs”) with the National Hydrocarbons Commission (“CNH”), Mexico’s oil and gas regulator.

12

The PSCs for our blocks include a cost recovery feature pursuant to which eligible costs in relation to the minimum work program activities are recoverable in-kind at a rate of 125% of costs from future production volumes. Production volumes are allocated in-kind between the consortium and the United Mexican States on a monthly basis based on the contractual value of the hydrocarbons as defined in the PSC. Up to 60% of the monthly contractual value of the hydrocarbons will be allocated to the consortium to recover eligible costs incurred in petroleum activities. Eligible costs exceeding 60% of the current month contractual value of the hydrocarbons will be recoverable in future periods. The amount of royalties will be determined for each type of hydrocarbons (oil, associated natural gas, non-associated natural gas and condensate) using an initial rate, adjusted thereafter for inflation. The remaining value of the hydrocarbons after the allocation for cost recovery and royalties is considered operating profit under the PSC. The allocation of operating profit to the consortium after the allocation for cost recovery and royalties on Blocks 7 and 31 is 31% and 35%, respectively. The profit for oil and gas is determined on a monthly basis using an adjustment mechanism based on the projects rate of return (“ROR”). In the event that the cumulative project’s ROR in any one month exceeds 25%, the barrels of oil allocated to the consortium after cost recovery are reduced on a sliding scale. Once the cumulative project’s internal ROR meets or exceeds 40%, the reduction locks in at a maximum rate. The Hydrocarbons Revenue Law provides that exploration and extraction activities are zero rated for value-added tax (“VAT”) purposes; all other activities are taxed at 16% VAT. The 0% rates only apply to agreements between the United Mexican States and state-owned enterprises or entities, and do not apply to any other agreement executed with third parties, even in the case of exploration and extraction contracts. The Mexico income tax rate is 30%.

As of December 31, 2020, our core areas in Mexico are illustrated below:

Block 7 — In July 2017, we completed drilling operations on the offshore Mexico Zama-1 exploration well. The Zama-1 well is the first offshore exploration well to be drilled in Mexico by the private sector. Well results confirmed the base of the reservoir section, with no penetration of an oil-water contact. The gross oil bearing interval is over 1,100 feet with petrophysical data indicating excellent rock properties and an oil sample with 30 degree API gravity oil. The well has been suspended as a future producer.

In the fourth quarter of 2018, we spud the Zama-2 well, the first appraisal well to be drilled in the field. The Zama-2 well confirmed the results of the original Zama-1 exploration well. In the first quarter of 2019, we drilled the second appraisal penetration, the Zama-2 ST1 well, which successfully tested the northern limits of the reservoir, acquired over 700 feet of whole core to collect detailed rock properties and performed successful well tests in several perforated intervals, reaching an unstimulated and restricted combined production rate of 8.2 MBoepd gross, of which 95% was oil.

13

In the second quarter of 2019, we concluded our three well appraisal of the Zama discovery. The Zama-3 well was drilled to test the southern extent of the reservoir. Well results included the capturing of approximately 717 feet of whole core.

Front-end engineering & design work is advancing to optimize the recovery and economic development of the field and allow for the earliest possible initial production date. We have significantly narrowed the number of potential development concepts and the prevailing concept design will be the basis for the development. We were also granted a two-year contract term extension as well as regulatory approvals to allow for exploration activities on additional retained acreage in Block 7 that are separate and incremental to the Zama discovery. See Part IV, Item 15. Exhibits, Financial Statement Schedules — Note 4 — Property, Plant and Equipment for further detail on our Mexico properties.

In September 2018, we and our consortium partners in Block 7 signed a Pre-Unitization Agreement (“PUA”) with Pemex Exploracion y Produccion (“Pemex”) related to certain tracts within the Amoca-Yaxche-03 allocation and the contiguous Block 7 PSC. Both areas are situated in the offshore portion of the Sureste Basin. The two year PUA enabled information sharing related to the Zama discovery and potential extension into Pemex’s neighboring block. The PUA was approved by the Mexican Secretariat of Energy (“SENER”) and on July 7, 2020, we received a notice from SENER instructing the partners of Block 7 and Pemex to unitize the Zama Field. The formal notice established a firm deadline by which the parties should act in good faith to finalize the unit agreement for the Zama Field, which is expected to be signed in 2021. Once the unit agreement is signed, the Zama Field Development Plan, which we are currently preparing, can be submitted to CNH for approval. Our participation interest (“PI”) in Block 7 is 35%, and we are the operator.

Block 31— In September 2018, we entered into a transaction (the “Hokchi Cross Assignment”) with Hokchi Energy, S.A. de C.V. (“Hokchi”), a subsidiary of Pan American Energy LLC (“PAE”), to cross assign 25% PIs in our Block 2 and their Block 31. Our assignment of a 25% PI in Block 2 to Hokchi closed on December 21, 2018, and Hokchi’s assignment of a 25% PI in Block 31 to us closed on May 22, 2019. Following the completion of the Hokchi Cross Assignment, we owned a 25% PI in Block 31, and Hokchi was the operator.

In July 2019, we spud the first project on Block 31, the Xaxamani-2EXP well. This is the first well in the Xaxamani project area, which is a shallow oil project set up by the Xaxamani-1 exploratory well drilled in 2003, which logged oil pay in several intervals. Also in the third quarter of 2019, PAE drilled the exploratory well, Tolteca-1EXP. A successful drill-stem test on the Xaxamani-2EXP confirmed productivity by producing oil to the surface. The two-well drilling campaign further confirmed the oil and gas discovery. The discovery is in very shallow waters and is less than two miles from shore. We hold a 25% PI in Block 31.

14

Summary of Reserves

The following table summarizes our estimated proved reserves as of December 31, 2020, 2019 and 2018, which are all located in the United States.

Reconciliation of Standardized Measure to PV-10

PV-10 is a non-GAAP financial measure and differs from the standardized measure of discounted future net cash flows, which is the most directly comparable GAAP financial measure. PV-10 is a computation of the standardized measure of discounted future net cash flows on a pre-tax basis. PV-10 is equal to the standardized measure of discounted future net cash flows at the applicable date, before deducting future income taxes, discounted at 10 percent. We believe that the presentation of PV-10 is relevant and useful to investors because it presents the discounted future net cash flows attributable to our estimated net proved reserves prior to taking into account future corporate income taxes, and it is a useful measure for evaluating the relative monetary significance of our oil and natural gas properties. Further, investors may utilize the measure as a basis for comparison of the relative size and value of our reserves to other companies without regard to the specific tax characteristics of such entities. We use this measure when assessing the potential return on investment related to our oil and natural gas properties. PV-10, however, is not a substitute for the standardized measure of discounted future net cash flows. Our PV-10 measure and the standardized measure of discounted future net cash flows do not purport to represent the fair value of our oil and natural gas reserves.

The following table provides a reconciliation of the standardized measure of discounted future net cash flows to PV-10 of our proved reserves at December 31, 2020, 2019 and 2018 (in thousands).

15

Changes in Proved Developed Reserves

The following table discloses our estimated changes in proved developed reserves during the year ended December 31, 2020:

Revisions of Previous Estimates — Downward revisions of 12.2 MMBoe are primarily attributable to a decrease in commodity prices and differentials across our core areas and 2.9 MMBoe of performance revisions in the Green Canyon core area.

Additions — Additions of 4.7 MMBoe are primarily attributable to the successful drilling in the Claiborne Field located in the Mississippi Canyon core area and Green Canyon 18 Field located in the Green Canyon core area.

Acquired — Acquired proved developed reserves of 49.4 MMBoe are attributable to the ILX and Castex Acquisition, the Castex 2005 Acquisition and the LLOG Acquisition located within the Mississippi Canyon and the Shelf and Gulf Coast core area. See Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional information regarding each of our acquisitions.

Development of Proved Undeveloped Reserves

The following table discloses our estimated proved undeveloped (“PUD”) reserve activities during the year ended December 31, 2020:

Our PUD reserves at December 31, 2020 decreased by 7.8 MMBoe, or 18% primarily due to:

Revisions of Previous Estimates — Downward revisions of 12.0 MMBoe are primarily attributable to a decrease in commodity prices and differentials across our core areas and 3.2 MMBoe of technical revisions.

Acquired — Acquisitions of 11.4 MMBoe of PUD reserves are attributable to the ILX and Castex Acquisition located within the Mississippi Canyon and the Shelf and Gulf Coast core area.

Conversion to Proved Developed Producing — During 2020, we converted 7.2 MMBoe of proved undeveloped reserves to proved developed primarily attributable to successful platform drilling rig campaign in our Green Canyon 18 Field located in the Green Canyon core area.

16

We annually review all PUD reserves to ensure an appropriate plan for development exists. Our PUD reserves are required to be converted to proved developed reserves within five years of the date they are first booked as PUD reserves. Future development costs associated with our PUD reserves at December 31, 2020 totaled approximately $315.5 million, of which $289.0 million is attributable to the Mississippi Canyon and Green Canyon core areas. When considering capital expenditures associated with other exploration projects and abandonment obligations, we expect to fund the development of PUD reserves using cash flows from operations and, if needed, availability under the Company’s senior reserve-based revolving credit facility (the “Bank Credit Facility”), in each future annual period prior to the five year expiration. Our 2021 drilling program includes development of PUD reserves, and the conversion rate may not be uniform due to obligatory wells, newly acquired PUD reserves and production performance targets.

Internal Controls over Reserve Estimates and Reserve Estimation Procedures

At December 31, 2020, 2019 and 2018, proved oil, natural gas and NGL reserves attributable to our net interests in oil and natural gas properties were estimated and compiled for reporting purposes by our reservoir engineers and audited by Netherland, Sewell & Associates, Inc. (“NSAI”), independent petroleum engineers and geologists, as described in further detail below.

Our policies regarding internal controls over the determination of reserves estimates require reserves quantities, reserves categorization, future producing rates, future net revenue and the present value of such future net revenue prepared using the definitions set forth in Regulation S-X, Rule 4-10(a) and subsequent SEC staff interpretations and guidance. These internal controls, which are intended to ensure reliability of our reserves estimations, include, but are not limited to, the following:

|

| • | Reserve information, as well as models used to estimate such reserves, is stored on secure database applications to which only authorized personnel are given access rights consistent with their assigned job function. |

|

| • | A comparison of historical expenses is made to the lease operating costs in the reserve database. |

|

| • | Internal reserves estimates are reviewed by well and by area by our reservoir engineers. A variance analysis by well to the previous year-end reserve report is performed. |

|

| • | Reserve estimates are reviewed and approved by certain members of senior management, including our President and Chief Executive Officer. |

|

| • | We engaged NSAI to perform an independent audit of our processes and the reasonableness of our estimates of proved reserves at December 31, 2020, 2019 and 2018. Our management requires that the independent petroleum engineers and geologists and our reserve quantities and calculation of the net present value of the reserves, collectively, vary by no more than 10% in the aggregate, in accordance with Society of Petroleum Evaluation Engineers (“SPEE”) auditing standards. |

|

| • | Data is transferred to NSAI through a secure file transfer protocol site. |

|

| • | Material reserve variances are discussed among NSAI, as applicable, our internal reservoir engineers and our Director of Reserves to ensure the best estimate of remaining reserves. |

Because these estimates depend on many assumptions, any or all of which may differ substantially from actual results, reserve estimates may be different from the quantities of oil, natural gas and NGLs that are ultimately recovered.

17

During the reserves audit, NSAI did not independently verify the accuracy and completeness of information and data furnished by us with respect to ownership interests, oil, natural gas and NGL production, well test data, historical costs of operation and development, product prices or any agreements relating to current and future operations of the fields and sales of production. However, if in the course of the examination something came to the attention of NSAI that brought into question the validity or sufficiency of any such information or data, NSAI did not rely on such information or data until it had satisfactorily resolved its questions relating thereto or had independently verified such information or data. When compared on a well by well basis, some of our estimates are greater and some are less than the estimates of NSAI. Given the inherent uncertainties and judgments that go into estimating proved reserves, differences between internal and external estimates are to be expected. NSAI determined that its estimates of reserves have been prepared in accordance with the definitions and regulations of the SEC, including the criteria of “reasonable certainty,” as it pertains to expectations about the recoverability of reserves in future years, under existing economic and operating conditions, consistent with the definition in Rule 4-10(a)(24) of Regulation S-X. NSAI issued unqualified audit opinions on our reserves as of December 31, 2020, 2019 and 2018 based upon its evaluations. NSAI concluded that our estimates of reserves were, in the aggregate, reasonable and have been prepared in accordance with Standards Pertaining to the Estimating and Auditing of Oil and Gas Reserves Information promulgated by the SPEE. The NSAI reports are filed as exhibits to this Annual Report.

Technologies Used in Reserve Estimation

The SEC’s reserves rules allow the use of techniques that have been proved effective by actual production from projects in the same reservoir or an analogous reservoir or by other evidence using reliable technology that establishes reasonable certainty. The term “reasonable certainty” implies a high degree of confidence that the quantities of oil, natural gas and/or NGLs actually recovered will equal or exceed the estimate. To achieve reasonable certainty, our internal reservoir engineers employed technologies that have been demonstrated to yield results with consistency and repeatability. The technologies and economic data used in the estimation of our proved reserves include, but are not limited to, well logs, geologic maps, seismic data, well test data, production data, historical price and cost information and property ownership interests. The accuracy of the estimates of our reserves is a function of:

|

| • | the quality and quantity of available data and the engineering and geological interpretation of that data; |

|

| • | estimates regarding the amount and timing of future operating costs, development costs and workovers, all of which may vary considerably from actual results; |

|

| • | future prices of oil, natural gas and NGLs, which may vary considerably from those mandated by the SEC; and |

|

| • | the judgment of the persons preparing the estimates. |

Qualifications of Primary Internal Engineer

Our Director of Reserves is the technical person primarily responsible for overseeing the preparation of our internal reserve estimates and for coordinating reserve audits conducted by NSAI. He has over 46 years of industry experience with positions of increasing responsibility, including 38 years as a reserves evaluator or manager. His further professional qualifications include a State of Texas Professional Engineering License, extensive internal and external reserve training and asset evaluation. In addition, he is an active participant in industry reserve seminars and professional industry groups, and has been a member of the Society of Petroleum Engineers (“SPE”) for over 46 years. He reports directly to our Vice President of Corporate Development.

18

Drilling Activity

The following table sets forth our drilling activity during the years ended December 31, 2020, 2019 and 2018:

| (1) | A productive well is an exploratory or development well found to be capable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas producing well. Productive wells are included in the table in the year they were determined to be productive, as opposed to the year the well was drilled. |

| (2) | A dry well is an exploratory or development well that is not a productive well. Dry wells are included in the table in the year they were determined not to be productive, as opposed to the year the well was drilled. |

| (3) | 1 gross and net development well had a dual completion in an exploratory zone. |

As of December 31, 2020, we had wells actively drilling or completing and wells suspended or awaiting completion, as follows:

Productive Wells

The number of our productive wells is as follows for the year ended December 31, 2020:

| (1) | Includes 8.0 gross and 8.0 net wells with dual completions. |

19

Acreage

Gross and net developed and undeveloped acreage is as follows for the year ended December 31, 2020:

Undeveloped acreage is considered to be those leased acres on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether or not such acreage contains proved reserves. Included within undeveloped acreage are those leased acres (held by production under the terms of a lease) that are not within the spacing unit containing, or acreage assigned to, the productive well holding such lease. The terms of our leases on undeveloped acreage as of December 31, 2020 are scheduled to expire as shown in the table below (the terms of which may be extended by drilling and production operations):

Crude Oil, Natural Gas and NGL Production, Prices and Production Costs

Our production volumes, average sales prices and average production costs are as follows:

20

Crude Oil, Natural Gas and NGL Production, Prices and Production Costs—Significant Fields

Green Canyon Core Area — Phoenix Field

The following table sets forth certain information regarding our production volumes, average sales prices and average production costs for the Phoenix Field, which consisted of 15% or more of our total estimated proved reserves at December 31, 2020, 2019 and 2018:

Mississippi Canyon Core Area — Pompano Field

The following table sets forth certain information regarding our production volumes, average sales prices and average production costs for the Pompano Field, which consisted of 15% or more of our total estimated proved reserves at December 31, 2020, 2019 and 2018:

| (1) | The year ended December 31, 2018 includes the period from the closing date of the Stone Combination from May 10, 2018, through December 31, 2018. |

Expenditures and Costs Incurred

For information on property development, exploration and acquisition costs, see Part IV, Item 15. Exhibits, Financial Statement Schedules — Note 14 — Supplemental Oil and Gas Disclosures (Unaudited).

21

Title to Properties

We believe that we have satisfactory title to our oil and natural gas properties in accordance with generally accepted industry standards. Individual properties may be subject to burdens such as royalties, overriding royalties, and carried, net profits, working and other outstanding interests customary in the industry. In addition, interests may be subject to obligations or duties under applicable laws or burdens such as production payments, ordinary course liens incidental to operating agreements and for current taxes and development obligations under oil and natural gas leases. As is customary in the industry in the case of undeveloped properties, often limited investigation of record title is made at the time of acquisition. Title search investigations are made prior to the consummation of an acquisition of producing properties and before commencement of drilling operations on undeveloped properties. To the extent title opinions or other investigations reflect defects affecting such undeveloped properties, we are typically responsible for curing any such title defects at our expense.

Commodity Price Risks and Price Risk Management Activities

Production from our properties is marketed using methods that are consistent with industry practices. Sales prices for oil and natural gas production are negotiated based on factors normally considered in the industry, such as an index or spot price, price regulations, distance from the well to the pipeline, commodity quality and prevailing supply and demand conditions. We enter into derivative contracts on our oil and natural gas production primarily to stabilize cash flows and reduce the risk and financial impact of downward commodity price movements on commodity sales. For additional information regarding our commodity price risk and commodity derivative instruments, see Part II, Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

Significant Customers

Oil and natural gas companies spend capital on exploration, drilling and production operations expenditures, the amount of which is generally dependent on the prevailing view of future oil and natural gas prices which are subject to many external factors which may contribute to significant volatility in future prices. We market substantially all of our oil, natural gas and NGL production from the properties we operate and those we do not operate. Our customers consist primarily of major oil and gas companies, well-established oil and pipeline companies and independent oil and natural gas producers and suppliers. We perform ongoing credit evaluations of our customers and provide allowances for probable credit losses when necessary. For the year ended December 31, 2020, 47%, 22%, and 12% of our oil, natural gas and NGL revenues were attributable to Shell Trading (US) Company, Phillips 66 and Chevron Products Company, respectively, which are the customers that individually represented 10% or more of our oil, natural gas and NGL revenues.

Competitive Conditions

The oil and natural gas business is highly competitive in the exploration for and acquisition of reserves, the acquisition of oil and natural gas leases, equipment and personnel required to find and produce reserves and in the gathering and marketing of oil, natural gas and NGLs. We compete with large integrated oil and natural gas companies as well as independent exploration and production companies. Certain of our competitors may have significantly more financial or other resources available to them. In addition, certain of the larger integrated companies may be better able to respond to industry changes, including price fluctuation, oil and natural gas demand and governmental regulations.

However, we believe our high quality oil-weighted production base, proven expertise in utilizing seismic technology to identify, evaluate and develop exploitation and exploration opportunities, balanced mix of assets in the U.S. Gulf of Mexico deep and shallow waters and significant operating control give us a strong competitive position relative to many of our competitors.

Seasonality of Business

Weather conditions affect the demand for, and prices of, oil and natural gas. Due to these seasonal fluctuations, our results of operations for individual quarterly periods may not be indicative of the results that may be realized on an annual basis. Generally, but not always, the demand for gas decreases during the summer months and increases during the winter months. Seasonal anomalies such as mild winters or hot summers may impact general seasonal changes in demand.

22

Insurance Matters

Our oil and natural gas operations are subject to risks incident to the operation of oil and gas wells, including but not limited to uncontrolled flows of oil, gas, brine or well fluids into the environment, blowouts, cratering, mechanical difficulties, fires, explosions or other physical damage, pollution or other risks, any of which could result in substantial losses to us. In addition, our oil and natural gas properties are located in the U.S. Gulf of Mexico, which makes us more vulnerable to tropical storms and hurricanes. These hazards can cause personal injury or loss of life, severe damage to and destruction of property and equipment, pollution or environmental damage and the suspension of operations. Damages arising from such occurrences may result in lawsuits asserting large claims. Insurance may not be sufficient or effective under all circumstances or against all hazards to which we may be subject. A successful claim for which we are not fully insured could have a material adverse effect on our financial condition, results of operations and cash flow. Although we obtain insurance against some of these risks, we cannot insure against all possible losses. As a result, any damage or loss not covered by insurance could have a material adverse effect on our financial condition, results of operations and cash flow.

We have insurance policies to cover some of our risk of loss associated with our operations, and we maintain the amount of insurance we believe is prudent. However, not all of our business activities can be insured at the levels we desire because of either limited market availability or unfavorable economics (limited coverage for the underlying cost).

Our general property damage insurance provides varying ranges of coverage based upon several factors, including well counts and the cost of replacement facilities. Our general liability insurance program provides a limit of $500 million for each occurrence and in the aggregate, and includes varying deductibles. Our Offshore Pollution Act insurance is subject to a maximum of up to $150 million for each occurrence and in the aggregate, including a $100,000 retention. Coverage is provided for damage to our assets resulting from a named U.S. Gulf of Mexico windstorm; however, such coverage is subject to a maximum of $170 million per named windstorm and in the aggregate, and is also subject to a maximum of $35 million per occurrence retention. We separately maintain an operators extra expense policy with additional coverage for an amount up to $500 million for U.S. Gulf of Mexico deepwater drilling wells, $150 million for U.S. Gulf of Mexico shelf drilling wells, $75 million for U.S. Gulf of Mexico producing and shut-in wells, $75 million for drilling and workover in inland waters and $25 million for drilling and workover in onshore fields that would cover costs involved in making a well safe after a blow-out or getting the well under control; re-drilling a well to the depth reached prior to the well being out of control or blown out; costs for plugging and abandoning the well; and costs for clean-up and containment and for damages caused by contamination and pollution. For our Mexico insurance policies, we maintain $250 million in operators extra expense coverage for operations and $500 million per occurrence and aggregate limit for general liability.

We may increase or decrease insurance coverage around our key strategic assets, including potentially purchasing catastrophic bond instruments. Our highest value assets, which are located in the Phoenix Field, produce through the HP-I floating production system, which has the capability to disconnect and move away in the event of a storm, mitigating the risk of property damage.

We customarily have reciprocal agreements with our customers and vendors in which each contracting party is responsible for its respective personnel for liability related to work performed for us. Under these agreements, we generally are indemnified against third party claims related to the injury or death of our customers’ or vendors’ personnel, subject to the application of various states’ laws.

23

Government Regulation

Exploration and development and the production and sale of oil, natural gas and NGLs are subject to extensive federal, state, local and foreign laws and regulations. An overview of these legal requirements is set forth below. Historically, our compliance with existing requirements has not had a material adverse effect on our financial position, results of operations or cash flows. However, current regulatory requirements may change, currently unforeseen environmental incidents may occur or past non-compliance with environmental laws or regulations may be discovered. Because such laws and regulations are frequently amended or reinterpreted, we are unable to predict the future cost or impact of complying with such laws. Although the regulatory burden on the oil and natural gas industry increases our cost of doing business and, consequently, affects our profitability, these burdens generally do not affect us any differently or to any greater or lesser extent than they affect others in our industry with similar types, quantities and locations of production.

General Overview — Our oil and natural gas operations are subject to various federal, state, local and foreign laws and regulations. Generally speaking, these regulations relate to matters that include, but are not limited to:

|

| • | location of wells; |

|

| • | size of drilling and spacing units or proration units; |

|

| • | number of wells that may be drilled in a unit; |

|

| • | unitization or pooling of oil and natural gas properties; |

|

| • | drilling and casing of wells; |

|

| • | issuance of permits in connection with exploration, drilling and production; |

|

| • | well production; |

|

| • | spill prevention plans; |

|

| • | protection of private and public surface and ground water supplies; |

|

| • | emissions permitting or limitations; |

|

| • | protection of endangered species; |

|

| • | use, transportation, storage and disposal of fluids and materials incidental to oil and natural gas operations; |

|

| • | surface usage and the restoration of properties upon which wells have been drilled; |

|

| • | calculation and disbursement of royalty payments and production taxes; |

|

| • | requirements for the posting of supplemental bonds or providing other forms of financial assurance for the plugging and abandonment of wells located in the U.S. Gulf of Mexico and offshore Mexico and, following cessation of operations, the removal or appropriate abandonment of all production facilities, structures and pipelines in those areas (“P&A” or “decommissioning” obligations); |

|

| • | performance of P&A obligations; and |

|

| • | transportation of production. |

Outer Continental Shelf (“OCS”) Regulation — Our operations on federal oil and natural gas leases in the U.S. Gulf of Mexico are subject to regulation by the Bureau of Safety and Environmental Enforcement (“BSEE”), the Bureau of Ocean Energy Management (“BOEM”) and the Office of Natural Resources Revenue (“ONRR”), which are all agencies of the U.S. Department of the Interior (“DOI”). These leases are awarded by the BOEM based on competitive bidding and contain relatively standardized terms and require compliance with detailed BSEE and BOEM regulations and orders issued pursuant to various federal laws, including the federal Outer Continental Shelf Lands Acts (“OCSLA”). For offshore operations, lessees must obtain BOEM approval for exploration, development and production plans prior to the commencement of their operations. In addition to permits required from other agencies such as the U.S. Environmental Protection Agency (“EPA”), lessees must obtain a permit from BSEE prior to the commencement of drilling and comply with regulations governing, among other things, engineering and construction specifications for production facilities, safety procedures, P&A of wells on the OCS, calculation of royalty payments and the valuation of production for this purpose, and removal of facilities.

24

Recent orders issued under the new Biden Administration have served to temporarily halt new leasing and new drilling opportunities on the OCS, which specifically excludes authorizations associated with existing operations under valid leases. In particular, the Acting Secretary of the U.S. Department of the Interior under the Biden Administration issued an order on January 20, 2021, effective immediately, that suspends the delegation of authority to the bureaus and agencies of the DOI to approve any new oil and gas leases and new drilling permits on federal lands and offshore waters, including the OCS for a period of 60 days. Building on this suspension, President Biden issued an executive order on January 27, 2021 that suspends new leasing activities for oil and gas exploration and production on federal lands and offshore waters pending review and reconsideration of federal oil and gas permitting and leasing practices. While the January 27, 2021 order does not apply to existing leases, the January 27, 2021 order further directs applicable agencies to take measures to eliminate provision of subsidies to the fossil fuel industry from budget requests beginning in 2022.

Laws and regulations are subject to change, and the trend in the United States over the past decade has been for these governmental agencies to continue to evaluate and as necessary develop and implement new, more restrictive safety, permitting and performance requirements, although in recent years under the Trump Administration there have been actions seeking to mitigate certain of those more rigorous standards. For example, in 2016, BSEE under the Obama Administration published a final rule on well control that, among other things, imposed rigorous standards relating to the design, operation and maintenance of blow-out preventers, real-time monitoring of deepwater, high temperature, high pressure drilling activities, and enhanced reporting requirements. However, BSEE under the Trump Administration subsequently reconsidered the 2016 final rule and published final revisions to this rule that became effective in 2019 and, among other things, eliminated the requirement for a BSEE-approved verification organization for third parties providing certifications of certain critical well control functions. In another example, BSEE under the Obama Administration published a final rule in 2016 updating certain safety and pollution prevention equipment (e.g., subsea safety equipment, including blowout preventers) requirements for production safety equipment, including an obligation for independent third-party review and certification that safety and pollution prevention equipment is operational and functioning as designed in the most extreme conditions, but in 2018, BSEE amended this rule, rolling back a number of safety requirements including the third-party review and certification obligation.

With the change in Presidential Administrations in January 2021, it is possible that BSEE and/or BOEM may reconsider regulatory actions taken by the prior Administration and that they may seek to adopt additional, more stringent safety, permitting and performance requirements. Compliance with Biden Administration legislative, executive and regulatory actions or any other legal initiatives that impact oil and natural gas exploration, development and production activities on the OCS could result in significant costs, including increased capital expenditures and operating costs, and could adversely impact our business. In addition, under certain circumstances, BSEE may require our operations on federal leases to be suspended or terminated. Any such suspension or termination could adversely affect our financial condition and operations.

Furthermore, hurricanes in the Gulf of Mexico can have a significant impact on oil and natural gas operations. The effects from past hurricanes have included structural damage to fixed production facilities, semi-submersibles and jack-up drilling rigs. The BOEM and BSEE continue to be concerned about the loss of these facilities and rigs as well as the potential for catastrophic damage to key infrastructure and the resultant pollution from future storms. In an effort to reduce the potential for future damage, the BOEM and the BSEE have periodically issued guidance aimed at improving platform survivability by taking into account environmental and oceanic conditions in the design of platforms and related structures. It is possible that similar, if not more stringent, requirements will be issued by the BOEM and the BSEE for future hurricane seasons. New requirements, if any, could increase our operating costs and/or capital expenditures.

25

In addition, in order to cover the various decommissioning obligations of lessees on the OCS, the BOEM generally requires that lessees post some form of acceptable financial assurances that such obligations will be met, such as surety bonds. The cost of such bonds or other financial assurance can be substantial, and we can provide no assurance that we can continue to obtain bonds or other surety in all cases. The BOEM requires that lessees demonstrate financial strength and reliability according to its regulations and provide acceptable financial assurances to assure satisfaction of lease obligations, including decommissioning activities on the OCS. In 2016, the BOEM under the Obama Administration issued Notice to Lessees and Operators (“NTL”) #2016-N01 (“2016 NTL”) to clarify the procedures and guidelines that BOEM Regional Directors use to determine if and when additional financial assurances may be required for OCS leases, rights of way (“ROWs”) and rights of use and easement (“RUEs”). While the 2016 NTL became effective in September 2016, it was not fully implemented as the BOEM under the Trump Administration first extended indefinitely in 2017 implementation of the NTL and subsequently rescinded the NTL in the latter half of 2020. The Trump Administration instead elected to pursue a proposed rule published jointly by the BOEM and the BSEE in October 2020 that seeks to clarify and provide greater transparency to decommissioning and related financial assurance requirements imposed on oil and gas lessees (record title owners), sublessees (operating rights owners) and RUE and ROW grant holders conducting operations on the federal OCS. With the change in Presidential Administrations in January 2021, it is possible that the October 2020 proposed rule will not be implemented and that other, possibly more stringent, final assurance requirements may ultimately be imposed.

The future cost of compliance with respect to supplemental bonding, including the obligations imposed on us, whether as current or predecessor lessee or grant holder, as a result of the 2016 NTL, to the extent re-implemented or the October 2020 proposed rule, to the extent finalized, as well as to the provisions of any new, more stringent, NTLs or final rules on supplemental bonding published by the BOEM under the Biden Administration, could materially and adversely affect our financial condition, cash flows and results of operations. Moreover, the BOEM has the right to issue liability orders in the future, including if it determines there is a substantial risk of nonperformance of the interest holder’s decommissioning liabilities.

Regulation in Shallow Waters Off the Coast of Mexico — Our operations on oil and natural gas blocks in shallow waters off the coast of Mexico’s Veracruz and Tabasco states and in other Mexican offshore areas where we are assessing other exploration opportunities, are subject to regulation by SENER, the CNH and other Mexican regulatory bodies. The CNH is responsible for, among other things, overseeing the tender procedures for awarding contracts for the exploration and production of oil and natural gas in Mexican waters, managing and supervising contracts that have been awarded, and approving exploration and production plans. The PSCs that we and our consortium partners have entered into for the development of these acreages contain terms that impose on us the duty to comply with various laws and regulations. These laws and regulations govern, among other things, the exploration and exploitation of hydrocarbons (including certain national content requirements), the treatment, conveyance, marketing, transport and storage of petroleum, and requirements for industrial safety, operational security, and facility decommissioning. Failure to comply can result in the imposition of monetary penalties, revocation of permits, rescission of the relevant PSC, suspension of operations, and ordered decommissioning of offshore facilities and systems. The laws and regulations governing activities in the Mexican energy sector are relatively new, having been significantly reformed in 2013, and the legal regulatory framework continues to evolve as SENER, the CNH and other Mexican regulatory bodies issue new regulations and guidance. Such regulations are subject to change, and it is possible that SENER, the CNH or other Mexican regulatory bodies may impose new or revised requirements that could increase our operating costs and/or capital expenditures for operations in Mexican offshore waters.

Hydrocarbon Export Regulation in Mexico — Our operations on oil and natural gas blocks in shallow waters off the coast of Mexico’s Veracruz and Tabasco states, and in other Mexican offshore areas where we are assessing other exploration opportunities, are subject to regulation by SENER. Such regulations are subject to change, and it is possible that ASEA or other Mexican regulatory bodies may impose new or revised requirements that could increase our operating costs and/or capital expenditures for operations in Mexican offshore waters. For example, on December 26, 2020, SENER published new regulations affecting the granting of permits for the import and export of hydrocarbons. These new regulations impose additional constraints on permit applicants, and grant SENER more discretion in issuing, modifying, and revoking those permits. Previously, such permits would have a term of 20 years – the new regulations limit terms to 5 years, restrict extensions, and add new requirements.

26

Some oil and gas companies, and Amexhi, a trade group comprised of oil and gas operators in Mexico, have filed Amparo proceedings, seeking a declaration that such regulations are unconstitutional. In February 2021, a Federal Judge in Mexico granted a general injunction which temporarily blocks the enforceability of these new regulations.

Environmental and Occupational Safety and Health Regulations

We are subject to various federal, state, local and foreign regulations concerning occupational safety and health as well as the discharge of materials into, and the protection of, the environment. Environmental laws and regulations relate to, among other things:

|

| • | assessing the environmental impact of seismic acquisition, drilling or construction activities; |

|

| • | the generation, storage, transportation and disposal of waste materials; |

|

| • | the emission of certain gases into the atmosphere; |

|

| • | the monitoring, abandonment, reclamation and remediation of well and other sites, including sites of former operations; |

|

| • | various environmental permitting requirements, such as permits for wastewater discharges; |

|

| • | the development of emergency response and spill contingency plans; |

|

| • | specific operating criteria addressing worker protection; and |

|

| • | protection of private and public surface and ground water supplies. |

Based on regulatory trends and increasingly stringent laws, our capital expenditures and operating expenses related to the protection of the environment and safety and health compliance have increased over the years and it is possible such expenses will continue to increase under the Biden Administration. We cannot predict with any reasonable degree of certainty our future exposure concerning such matters, and the cost of compliance could be significant. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, the imposition of remedial obligations, natural resource damages or the issuance of injunctive relief (including orders to cease operations). Failure to comply with these laws and regulations can result in the assessment of administrative, civil or criminal penalties, the issuance of remedial obligations and the imposition of injunctions limiting or prohibiting certain of our operations. Both onshore and offshore drilling in certain areas has been opposed by environmental groups and, in certain areas, has been restricted. Additionally, President Biden has made the combat of climate change arising from GHG emissions a priority under his Administration and orders have already been issued to temporarily halt new leasing and new drilling opportunities, excluding authorizations for existing operations under valid leases, on the OCS, and additional orders or new legislative or regulatory initiatives regarding the restriction, delay or cancellation of such new or existing activities could be issued in the future. Moreover, some environmental laws and regulations may impose strict liability, which could subject us to liability for conduct that was lawful at the time it occurred or conduct or conditions caused by prior operators or third parties. To the extent laws are enacted or other governmental action is taken that prohibits or restricts onshore or offshore drilling or imposes environmental protection requirements that result in increased costs to the oil and gas industry in general, our business and financial results could be adversely affected. There are also increasing financial risks for fossil fuel producers as stockholders and bondholders currently invested in fossil-fuel energy companies concerned about the potential effects of climate change may elect in the future to shift some or all of their investments into non-fossil fuel energy related sectors.

We expect to continue making expenditures on a regular basis relating to environmental compliance. We maintain insurance coverage for spills, pollution and certain other environmental risks, although we are not fully insured against all such risks. Our insurance coverage provides for the reimbursement to us of certain costs incurred for the containment and clean-up of materials that may be suddenly and accidentally released in the course of our operations, but such insurance does not fully insure against pollution and similar environmental risks. We do not anticipate that we will be required under current environmental laws and regulations to expend amounts that will have a material adverse effect on our consolidated financial position or our results of operations. However, since environmental costs and liabilities are inherent in our operations and in the operations of companies engaged in similar businesses and since regulatory requirements frequently change and may become more stringent under the Biden Administration, there can be no assurance that material costs and liabilities will not be incurred in the future. Such costs may result in increased costs of operations and acquisitions and decreased production.

27

Water Discharges — Our discharges into waters of the United States are limited by the federal Clean Water Act, as amended (“CWA”), and analogous state laws. The CWA prohibits any discharge of pollutants, including spills and leaks of oil and other substances, into waters of the United States, except in compliance with permits issued by federal and state governmental agencies. These discharge permits also include monitoring and reporting obligations. Failure to comply with the CWA, including discharge limits set by permits issued pursuant to the CWA, may also result in administrative, civil or criminal enforcement actions. Violations of the CWA can result in suspension, debarment or the imposition of statutory disability, each of which prevents companies and individuals from participating in government contracts and receiving some non-procurement government benefits. The CWA also requires the preparation of oil spill response plans and spill prevention, control and countermeasure plans.

Oil Pollution Act — The Oil Pollution Act of 1990, as amended (“OPA”), holds owners and operators of offshore oil production or handling facilities, including the lessee or permittee of the area where an offshore facility is located, strictly liable for the costs of removing oil discharged into waters of the United States and for certain damages from such spills. OPA assigns joint and several strict liability, without regard to fault, to each liable party for all containment and oil removal costs and a variety of public and private damages including, but not limited to, the costs of responding to a release of oil, natural resource damages and economic damages suffered by persons adversely affected by an oil spill. Although defenses exist to the liability imposed by OPA, they are limited. OPA’s damages liability cap is currently $137.7 million; however, a party cannot take advantage of liability limits if a spill was caused by gross negligence or willful misconduct, resulted from violation of a federal safety, construction or operating regulation, or if the party failed to report a spill or cooperate fully in the clean-up. OPA also requires responsible parties to maintain evidence of financial responsibility in prescribed amounts. OPA currently requires a minimum financial responsibility demonstration of between $35 million to $150 million, based on a worst case oil spill discharge volume, for companies operating on the OCS, although the BOEM may increase this amount in certain situations, but in no event greater than $150 million. From time to time, the United States Congress has proposed, but not adopted, amendments to OPA raising the financial responsibility requirements. If OPA is amended to increase the minimum level of financial responsibility, we may experience difficulty in providing financial assurances sufficient to comply with this requirement. We cannot predict at this time whether OPA will be amended or whether the level of financial responsibility required for companies operating on the OCS will be increased. In any event, if an oil discharge or substantial threat of discharge were to occur, we may be liable for costs and damages, which costs and liabilities could be material to our results of operations and financial position. If an oil discharge or substantial threat of discharge were to occur, we could be liable for costs and damages, which costs and damages could be material to our results of operations and financial position.

National Environmental Policy Act — The National Environmental Policy Act, as amended (“NEPA”), requires federal agencies, including the DOI, to consider the impacts their actions have on the human environment, and to prepare detailed statements for major federal actions having the potential to significantly impact the environment. These requirements can lead to additional costs and delays in permitting for operators as the DOI or its bureaus may need to prepare Environmental Assessments (“EA”) and more detailed Environmental Impact Statements (“EIS”) in support of its leasing and other activities that have the potential to significantly affect the quality of the environment. If the EA indicates that no significant impact is likely, then the agency can release a finding of no significant impact and carry on with the proposed action. Otherwise, the agency must then conduct a full-scale EIS. On July 16, 2020, the Council on Environmental Quality (“CEQ”) under former President Trump’s Administration published a final rule modifying the NEPA. The modified final rule establishes a time limit of two years for preparation of EIS statements and one year for the preparation of EAs. The modified rule also eliminates the responsibility to consider cumulative effects of a project. The new regulations are subject to ongoing litigation in several federal district courts, and future implementation of the regulations is unclear. The NEPA process involves public input through comment. These comments, as well as the agency’s analysis of the proposed project, can result in changes to the nature of a proposed project, such as by limiting the scope of the project or requiring resource-specific mitigation. The adequacy of the agency’s NEPA process can be challenged in federal court by process participants. This process may result in delaying the permitting and development of projects, and result in increased costs.

28

Endangered Species Act — The Endangered Species Act, as amended (“ESA”), restricts activities that may affect federally identified endangered and threatened species or their habitats. Additionally, the Migratory Bird Treaty Act, as amended (“MBTA”), implements various treaties and conventions between the United States and certain other nations for the protection of migratory birds. Under the MBTA, the taking, killing or possessing of migratory birds is unlawful without a permit. The U.S. Fish and Wildlife Service (“FWS”) under former President Trump issued a final rule on January 7, 2021, which notably clarifies that criminal liability under the MBTA will apply only to actions “directed at” migratory birds, its nests or its eggs; however, in 2020, the U.S. District Court for the Southern District of New York vacated a Department of Interior memorandum articulating a similar interpretation. The Department of Interior under President Biden delayed the effective date of the January 2021 rule and opened a public comment period for further review. The Marine Mammal Protection Act, as amended (“MMPA”), similarly prohibits the taking of marine mammals without authorization. Additionally, the FWS may make determinations on the listing of species as threatened or endangered under the ESA and litigation with respect to the listing or non-listing of certain species may result in more fulsome protections for non-protected or lesser-protected species. We conduct operations on oil and natural gas leases in areas where certain species that are protected by the ESA, MBTA and MMPA are known to exist and where other species that could potentially be protected under these statutes are known to exist. The FWS or the National Marine Fisheries Service may designate critical habitat that it believes is necessary for survival of a threatened or endangered species. A critical habitat designation could result in further material restrictions to federal land use and may materially delay or prohibit access to protected areas for oil and natural gas development. These statutes may result in operating restrictions or a temporary, seasonal or permanent ban in affected areas.

Hazardous Substances and Waste Management — The Resource Conservation and Recovery Act, as amended (“RCRA”), generally regulates the disposal of solid and hazardous wastes and imposes certain environmental cleanup obligations. Although RCRA specifically excludes from the definition of hazardous waste “drilling fluids, produced waters and other wastes associated with the exploration, development or production of crude oil, natural gas or geothermal energy,” the EPA and state agencies may regulate these wastes as solid wastes. However, it is possible that certain oil and natural gas drilling and production wastes now classified as non-hazardous could be classified as hazardous wastes in the future. Any future loss of the RCRA exclusion for drilling fluids, produced waters and related wastes could result in increased costs to manage and dispose of generated wastes. Also, ordinary industrial wastes, such as paint wastes, waste solvents, laboratory wastes and waste oils, may be regulated as hazardous waste.

Comprehensive Environmental Response, Compensation and Liability Act — The Comprehensive Environmental Response, Compensation and Liability Act, as amended (“CERCLA”), and comparable state laws impose liability, without regard to fault or the legality of the original conduct, on persons that are considered to have contributed to the release of a “hazardous substance” into the environment. Such “responsible persons” may be subject to joint and several liability under CERCLA for the costs of cleaning up the hazardous substances that have been released into the environment and for damages to natural resources. Further, it is not uncommon for coastal landowners or other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment. In addition, we may adjust estimates of proved reserves to reflect production history, results of exploration and development, prevailing oil and natural gas prices and other factors, many of which are beyond our control.

Air Emissions — The Clean Air Act, as amended (“CAA”), and comparable state statutes restrict the emission of air pollutants and affect both onshore and offshore oil and natural gas operations. New facilities may be required to obtain separate construction and operating permits before construction work can begin or operations may start, and existing facilities may be required to incur capital costs in order to remain in compliance. Also, the EPA has developed, and continues to develop, more stringent regulations governing emissions of toxic air pollutants and is considering the regulation of additional air pollutants and air pollutant parameters. For example, in 2015, the EPA under the Obama Administration issued a final rule under the CAA, making the National Ambient Air Quality Standard (“NAAQS”) for ground-level ozone more stringent. Since that time, the EPA has issued area designations with respect to ground-level ozone and, more recently, in December 2020, the EPA, under the Trump Administration, published a final action that, upon conducting a periodic review of the ozone standard in accord with CAA requirements, elected to retain the 2015 ozone NAAQS without revision on a going-forward basis; however, several groups have filed litigation over this December 2020 decision, and this NAAQS standard may be subject to further revision under the Biden Administration. State implementation of the revised NAAQS could result in stricter permitting requirements, delay or prohibit our ability to obtain such permits and result in increased expenditures for pollution control equipment, the costs of which could be significant. State implementation of these revised air emission standards could result in stricter permitting requirements, delay, limit or prohibit our ability to obtain such permits, and result in increased expenditures for pollution control equipment, the costs of which could be significant.

29

Worker Health and Safety — The Occupational Safety and Health Act, as amended (“OSHA”), and comparable state statutes regulate the protection of the health and safety of workers. The OSHA hazard communication standard requires maintenance of information about hazardous materials used or produced in operations and provision of such information to employees. Other OSHA standards regulate specific worker safety aspects of our operations. Failure to comply with OSHA requirements can lead to the imposition of penalties.